Weekly S&P500 ChartStorm - 21 May 2023

This week: tech stock breakout, bearish/macro divergences, short squeeze, debt ceiling risk, bear market rallies, valuations, US vs global, profit margins, relative value trinity...

Welcome to the latest Weekly S&P500 #ChartStorm!

Learnings and conclusions from this week’s charts:

Tech stocks have broken out but face further lines of resistance overhead and must contend with bearish breadth (and macro) divergences.

Speculators remain heavily net short US equity index futures (similar levels as towards the end of the 2000’s bear and start of 2007/08 bear).

Bear market rallies can go bigger and longer than you might think.

Despite an initial reset, US equities are still very expensively priced vs history and vs global peers (bad for long-term investors, neutral for short-term traders).

EM equities are falling further behind vs US equities, risking an extension of the already decade+ relative bear market for EM vs USA.

Overall, despite a number of reasons for skepticism on the sustainability of the breakout in tech stocks, by itself it is a bullish development and likely sets the tone for the coming days and weeks even as the debt ceiling negotiations wear on. Further out though a number of question marks remain.

1. Tech Up: Perhaps the most interesting move in markets last week was the 3.5% gain in the Nasdaq, and this move now looks to be a clear departure from the Q2 range-trade for the Nasdaq. By itself it is a clearly bullish move and it will garner attention and chasing flows, but it is worth noting at least in passing that while one line of resistance has been cleared, many more lie ahead (it’s never that simple!). Also of interest is the lack of breakout in breadth (still seeing bearish divergence, it’s only the big stocks rallying).

Source: MarketCharts @Callum_Thomas

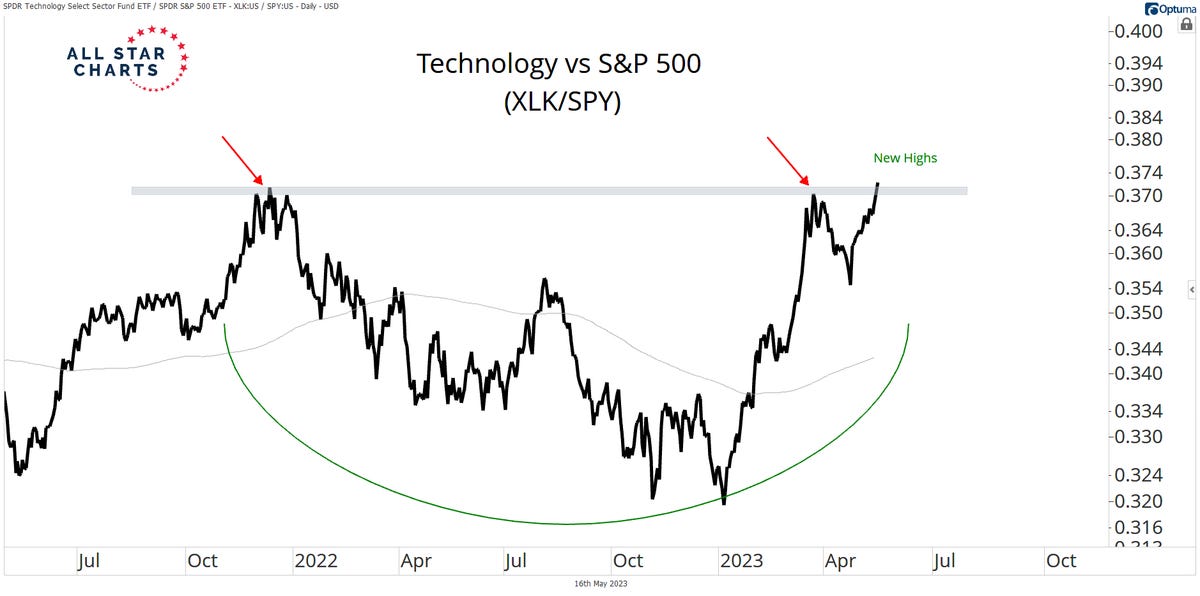

2. Tech Gaining the Upper Hand: Also of note is how tech is breaking out in relative terms vs the S&P500 (as the traditional cyclicals: financials, real estate, energy, materials all lose ground thanks to the commodity bear market and bank stress). Certainly one to keep an eye on as tech takes the lead.

Source: @AlfCharts

3. Macro Divergence: After trading in lockstep with bonds, the Nasdaq is now breaking away to its own path. Along with the bearish breadth divergence in the first chart, it does give reason for skepticism on the sustainability of the tech rally, but also raises the prospect of new narratives.

Source: @Stockspy1

4. Short Squeeze: On the other hand, we’re seeing heavy shorts in overall aggregated US index futures (net speculative positioning) — on a similar scale as was seen in the early-2000’s as the bear market was ending… but also similar to 2007 when the bear market was just getting started. The bullish take is that a short squeeze could take the market higher.

Source: @topdowncharts Topdown Charts

5. What About the Debt Ceiling? Well, it’s still there, and it’s still dragging on, and it’s still probably only going to get resolved either at or just past the last minute, as usual. So that brings us to a glance back at 2011 where the protracted bickering about the debt ceiling triggered S&P to do the almost unthinkable and downgrade the US sovereign credit rating…