Weekly S&P500 ChartStorm - 15 September 2024

This week: tech technicals, tech stock valuations, investment manager sentiment, Fed vs markets, bull market stats, earnings trends, yield curve, politics, and profit margins...

Welcome to the latest Weekly S&P500 #ChartStorm!

Learnings and conclusions from this week’s charts:

Tech-chop continues, choppy for longer…

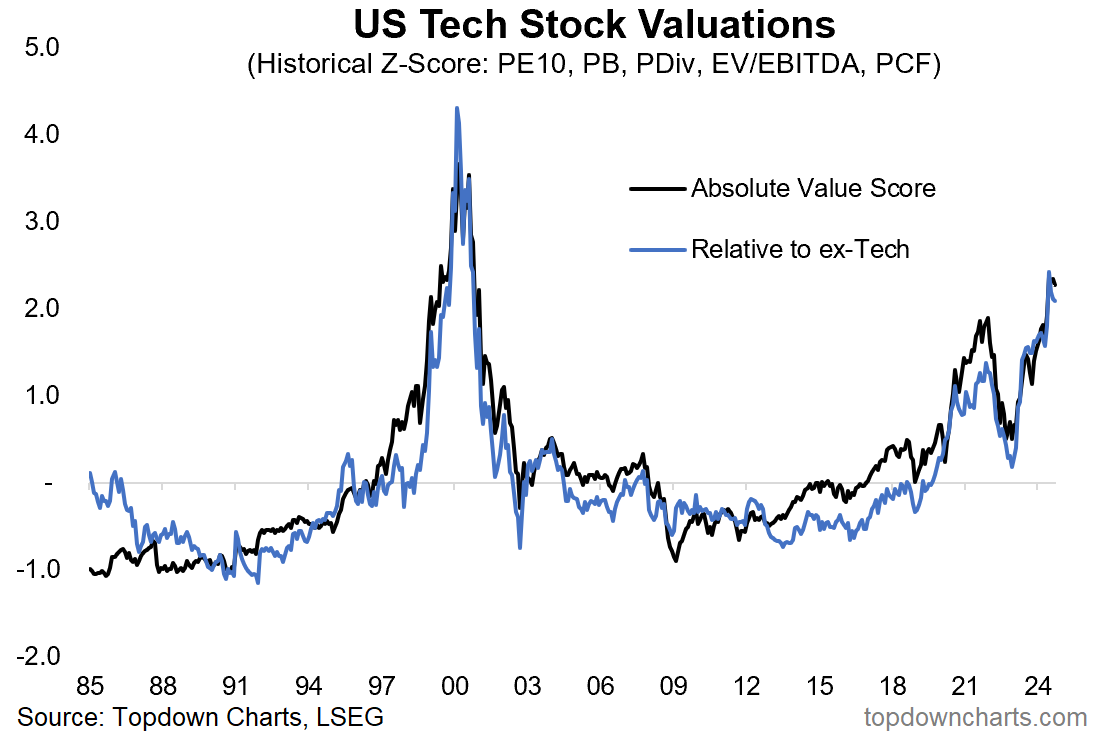

Tech stocks are extreme cheap vs the index.

Investment manager risk appetite has collapsed.

Yield curve un-inversions have a mixed track record.

Economics is more important than politics for investors.

Overall, while the S&P500 makes another close attempt at reclaiming the highs, tech stocks remain in chop-mode — no major breakdown, but no resolution of resistance, and as much points of weakness as strength. With valuations stretched and macro data mixed, it could turn at any point, but yet the trend is still up and rate cuts are set to begin this week, so let’s wait and see what the charts tell us…

1. Tech Chop: Another reprieve for tech last week with a bounce off support and the index still tracking comfortably above its upward sloping 200dma. However that resistance line still stands, the 50dma is looking rather wishy-washy, and 200dma breadth is trending lower (but importantly — holding above 50% for now). So it’s all a bit indecisive, no major breakdown, but no resolution of resistance either. Choppy for longer.

Source: Callum Thomas using MarketCharts.com Charting Tools

2. Tech Value: As a reminder, we care so intently about the tech technicals given the backdrop of extreme expensive valuations. The optimists will say that there’s still ample room to move until we get to the dot com bubble peak, or that it’s different this time (and it is — it is different, but also similar). The bears will remind us that when things are this stretched on the valuation front it doesn’t take much for it to turn and turn quickly. The pragmatists will say it looks risky but let’s watch for trigger points and technical confirmation before going full bear.

Source: 12 Charts to Watch in 2024 [Q3 Update]

3. Egregiously Expensive? Looking at the enterprise value to sales ratio for tech vs the index, it actually looks more stretched than the dot com bubble… but there’s a reason for that (see this week’s bonus chart for a clue!).

Source: Daily Chartbook

4. Lost Appetite: When it comes to risk sentiment it looks like investment managers have been consuming risk-taker’s ozempic — risk appetite has dropped to levels similar to when Russia invaded Ukraine and in 2023 during the SVB crisis. Clearly the mood has changed, and what’s driving it is a perfect storm of (geo)politics, concerns around expensive valuations, and mixed signals on the macro front. They are optimistic on central bank policy, but that’s not going to be a silver bullet for those other concerns.

Source: S&P Global Investment Manager Index

5. Friend of Fed: This is an interesting chart, it shows that usually after the first Fed rate cut the market rallies in the subsequent 12 months, and sometimes significantly. Curiously though there were back-to-back instances (2001, 2007) where this did *not* turn out to be the case. Goes to show that you can have a statistic and market rule humming along reliably for decades, and then reality confounds the historical probabilities. Will we get a rally this time?