Weekly S&P500 ChartStorm - 13 March 2022

This week: market positioning, tables and statistics, bear markets, volatility trends, oil headwinds, energy stocks, European equities, the themes theme, earnings share...

Welcome to the Weekly S&P500 #ChartStorm (by email!)

The Chart Storm is a weekly selection of 10 charts which I hand pick from around the web (+some of my own charts), and then post on Twitter.

The charts focus on the S&P500 (US equities); and the various forces and factors that influence the outlook - with the aim of bringing insight and perspective.

Hope you enjoy!

! ALERT ! Sign up to the (free) Chart of the Week over at the new Topdown Charts Substack entry-level service: Subscribe to the Chart of the Week

Each week we send you one of the most interesting charts on our radar, along with some commentary/context and a key takeaway — so you’re never left guessing on why the chart matters ...and the charts matter! The focus is on illuminating the ever-changing macro-market outlook to help identify incoming risks and opportunities. > > > Subscribe Now

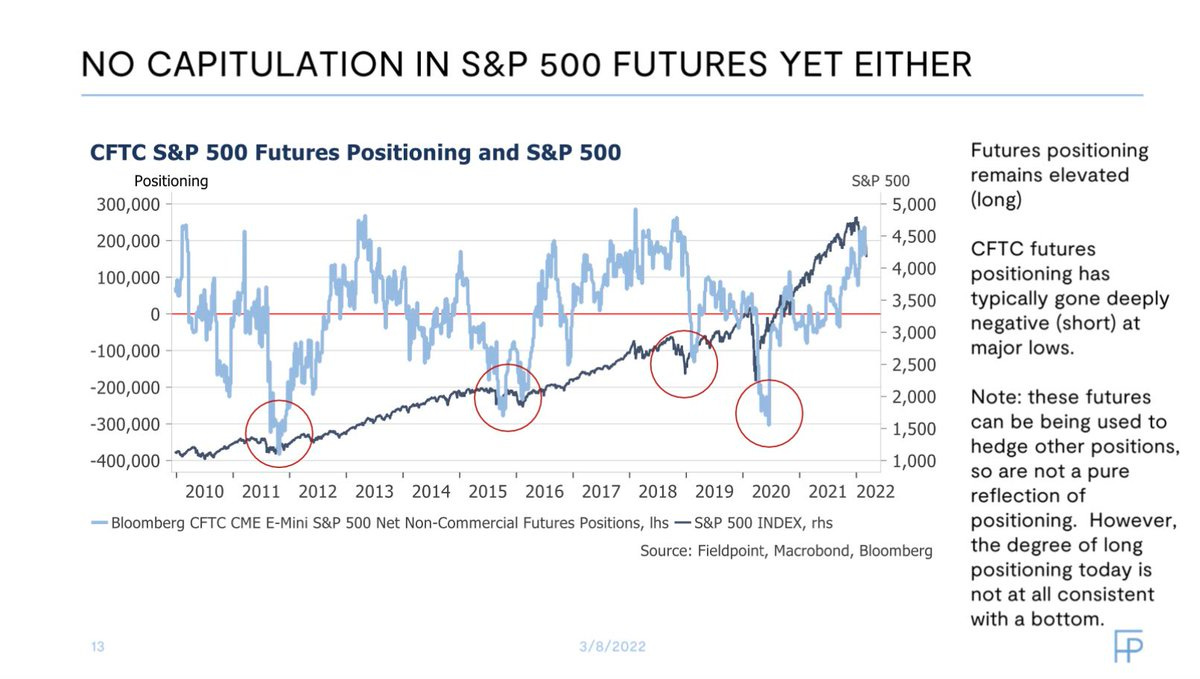

1. Speculative Futures Positioning: Always a lot of if's and but's when it comes to speculative futures positioning indicators like this (e.g. it might not be representative, or could reflect the other leg of some hedging or long/short trade, etc).

BUT, one thing is *very clear* -- this is not a picture of capitulation.

More evidence for: "feel kinda bearish, but still long".

Source: @CameronDawson

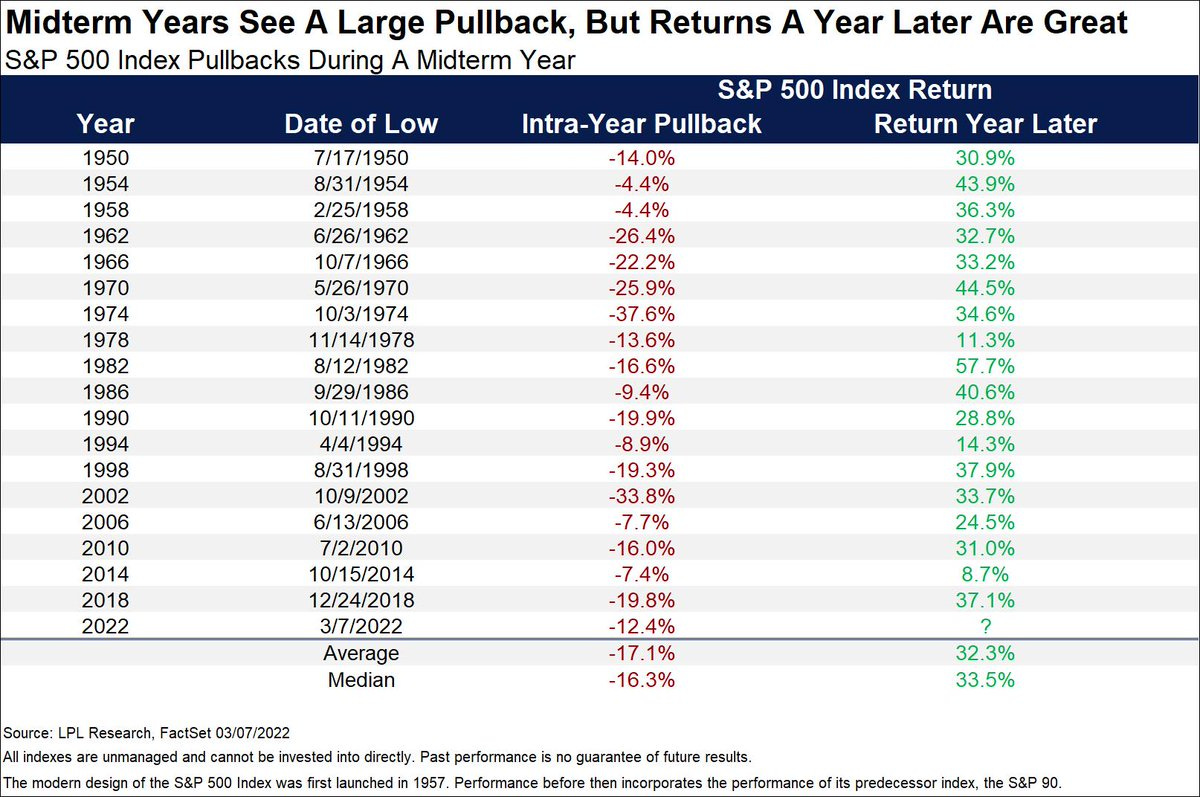

2. Midterm Malaise: One for the "this is normal and healthy" bucket...

It is not unusual to see a large pullback during mid-term years... (and in that destruction the creation of opportunities regularly happens).

Source: @RyanDetrick

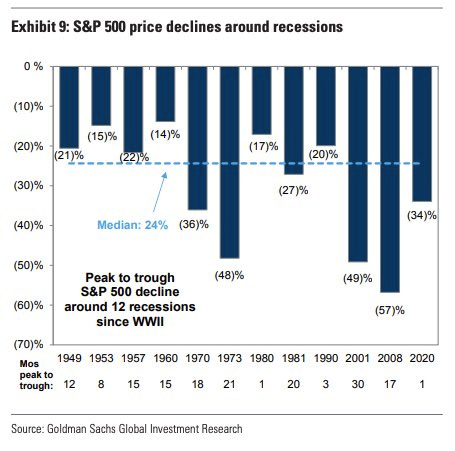

3. The Stockmarket *is* The Economy: Recessions expose the weak spots, destroy unsustainable models, and crush earnings. How this current stockmarket correction resolves (e.g. down then back to bull, vs down and down into bear market mode) will depend powerfully on whether a recession occurs.

(and it seems kinda likely, by my read)

Source: @MichaelAArouet

4. Bear Market History: Another table, basically a Friendly Reminder of what bear markets look like. (p.s. I wouldn't call covid a bear as such, it was a crash... bears are more sustained downturns in price which tend to be driven/reinforced by crappy macro etc -- rather than "dOwN 20% iS a bEaR mArKet!").

Source: @gnoble79

5. Regime Change? "Downside Volatility" is starting to dominate... a common feature of bear markets.

Source: @exposurerisk

6. Oil Shock: Just as central banks were already beginning to take the punchbowl away, oil comes in and dumps all over the earnings/economic outlook. To be absolutely clear (and the chart kind of speaks for itself): the surge in oil prices is a headwind to economic growth, earnings, and the stockmarket.

Source: @MrBlonde_macro

7. Energy Tho: Albeit, energy is of course a very different story.

(“stockmarket” vs market of stocks)

Source: @mark_ungewitter

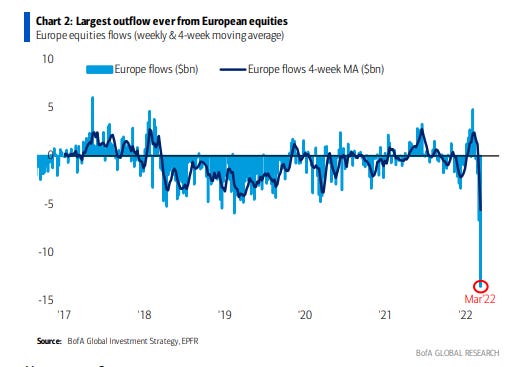

8. European Equity Exodus: European equities (understandably given direct geopolitical risk, not to mention indirect/direct economic + financial spillover risk) have been *heavily* sold... much much worse than during the pandemic panic.

Source: @MikeZaccardi

9. Also European Equities... Pockets of value out there, especially relative value.

Source: @ayeshatariq

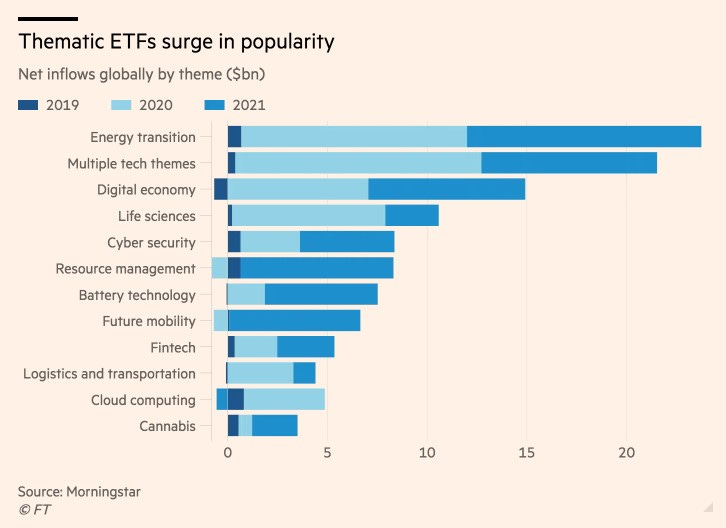

10. The Theme Age.

Source: @jessefelder

Thanks for following, I appreciate your interest!

oh… that’s right, almost forgot!

BONUS CHART >> got to include a goody for the goodies who subscribed.

The Rise and (?) of Tech: The market cap weighting of the tech and tech-related sectors has peaked, and its share of S&P 500 earnings has also begun to fall.

This chart shows the market cap weight + earnings share/weight in the S&P 500 of the Techy Sectors (after the big reclassification of 2018 which saw a bunch of tech stocks get rebranded into other sectors (thanks GICS), I felt it necessary to re-clump these back into a sort of super-sector).

Anyway, in many respects the chart kind of speaks for itself.

Yes, it is not dot-com/2000 in many respects, but there are many echoes. Probably the main takeaway is that it looks like the Techy Sectors have reached an upper limit in terms of earnings and market share domination of the S&P500, at least for now.

As for the why, it is important to highlight that the Techy Sectors group got a big one-off surge in growth when the pandemic forced a step-shift in a bunch of existing trends (e.g. online vs brick and mortar, work from home, small town vs big city, etc).

Meanwhile the other parts of the market took a big one-off hit as the real economy stopped and commodities crashed. That is changing now, at least and especially on the commodities and capex front.

This chart is therefore meaningful when it comes to the issue of rotation and sector allocations, but also in terms of the overall “stockmarket“ (i.e. the typical market-cap weighted index)… there were some clear excesses/pockets-of-stretch that likely need to be corrected through time and space(price).

—

Best regards,

Callum Thomas

SPONSOR: ( …he’s me!)

My research firm, Topdown Charts, has a new entry-level Substack service, which is designed to distill some of the key ideas and themes from the institutional fund manager service to provide the same high quality insights at a more accessible price.

Give it a try and let me know what you think