Weekly S&P500 ChartStorm - 1 September 2024

This week: monthly chart, bought the dip, euphoria, seasonal shiftiness, fundamental rotation, value opportunities, cap skews, deletions, defense, things in perspective...

Welcome to the latest Weekly S&P500 #ChartStorm!

Learnings and conclusions from this week’s charts:

The S&P 500 closed August *up* +2.3% on the month.

Retail bought the dip in August.

Sentiment is euphoric, but seasonal risks are rising.

Rotation prospects look good (value, fundamentals).

Buying index deletions has been a good strategy historically.

Overall, the heroic rebound in August belies the lingering issues facing macro and markets, and with (election year) seasonality now into the worst patch of the year, I would say it’s best not to get too complacent.

REMINDER: the new Weekly ChartStorm Chat-Room is now up and running — I will host a live Q&A session on Sunday evening about 7pm EST.

1. Onwards and Upwards: The S&P 500 closed August up +2.3% on the month (up 18.4% YTD) — leaving little-to-no evidence of the big VIX spike (to an intraday high of 65.73), the short-lived Japanese stockmarket crash, and geopolitics/recession fears which triggered a -6% pullback in the index earlier in the month.

Source: Topdown Charts

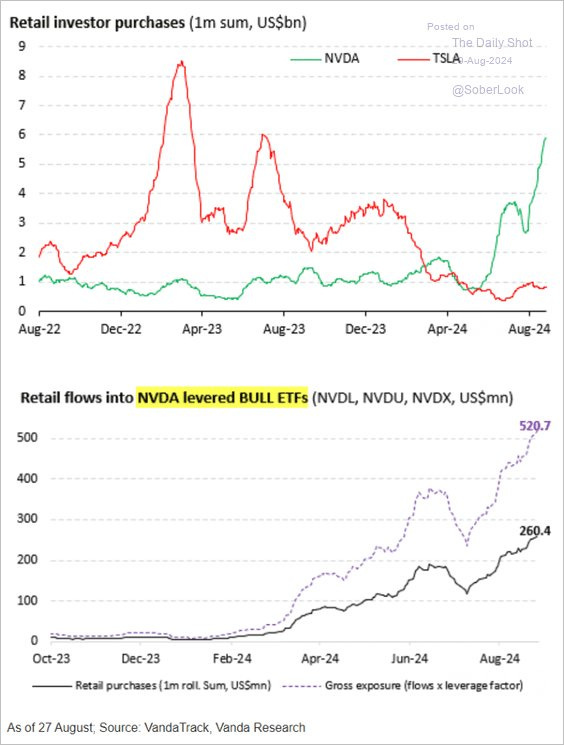

2. Dip Acquired: This is a fascinating chart, it shows the pivot in interest by retail from Tesla to Nvidia, but most importantly shows how it’s only really just recently that they have piled into NVDA in earnest. And fair enough, NVDA underwent about a 30% correction in the Jun-Aug period and is up about 20% off the lows. Buy the dip lives on — sentiment check: euphoria…

Source: DailyShot via Daily Chartbook

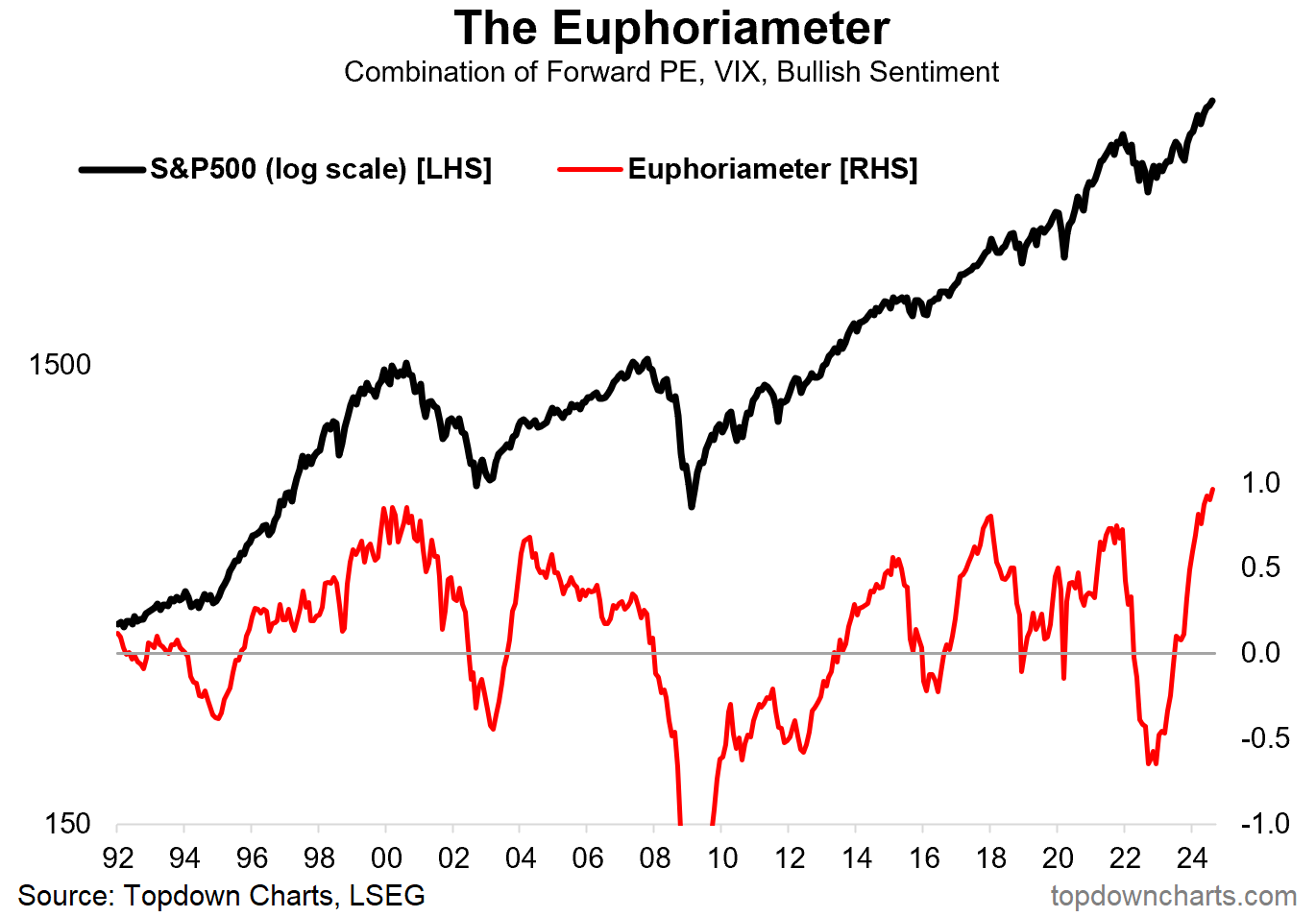

3. What Me Worry: My “Euphoriameter” indicator (which incorporates investor confidence signals from valuations, surveys, and risk pricing) not only shows no worries from the Aug-bust, but has actually gone on to new all-time highs. And why not? Investors got rewarded for buying the dip and the Fed is keen to keep the party going.

Source: Topdown Charts Professional

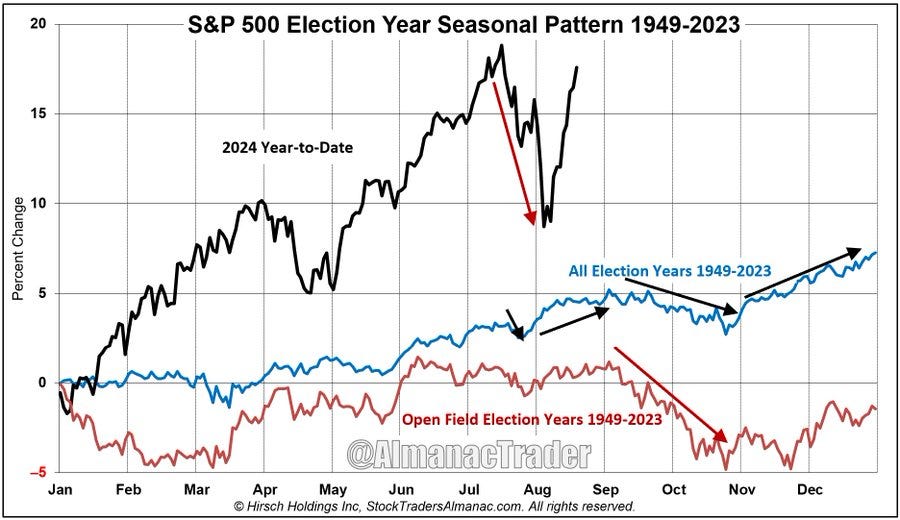

4. Season’s Greetings: One thing to be mindful of is the tendency for election years in particular to see seasonal weakness from now through to November (especially in open field years such as this one). I think this is a good playbook: sentiment is stretched, valuations high, geopolitical/economy risks elevated, and of course further noise and uncertainty around policy and politics as election crunch time approaches… and at this point on the Fed, with them confirming rate cuts incoming and everyone expecting a string of rate cuts and potentially large cuts, it’s theirs to disappoint.

Source: Humble Student of the Markets

5. Fundamental Rotation: Remember the rotation theme? Well don’t forget about it, because price rotations are more powerful when they have a fundamental driver — and with the “S&P 493” anticipated to start pulling more of their weight on earnings growth, I think we need to remain focused on rotation opportunities.

Source: @carlquintanilla

6. Deep Value: This chart tracks the valuations of the different cohorts in the market. Basically the most expensive stocks are more expensive than usual, while the cheapest stocks are much cheaper than usual. This speaks to the ebullient expectations priced-in for big tech (and risks to the index if those expectations get shaken), but also the absolute + relative value opportunities hiding in plain sight (rotation!).

Source: @MebFaber

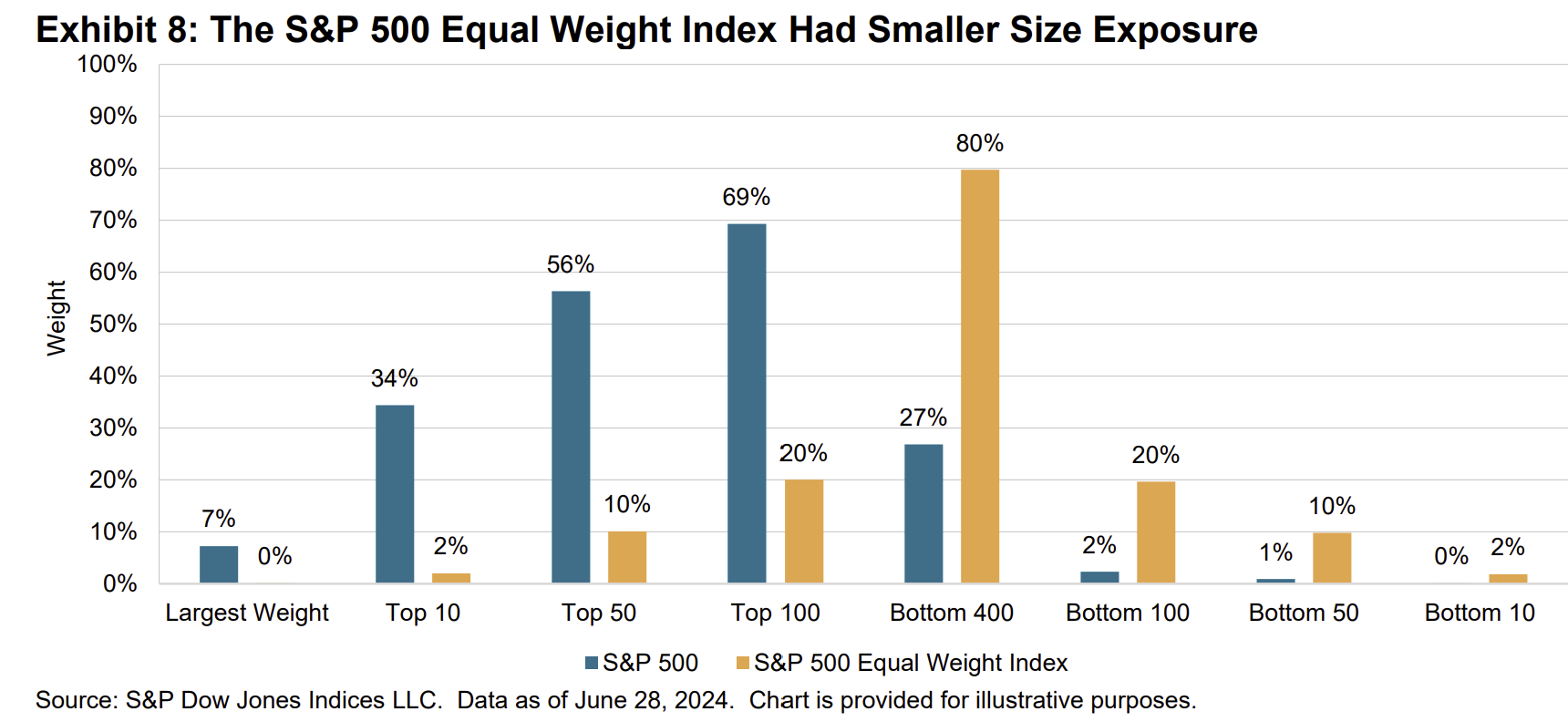

7. Equal vs Cap Weight: This is a novel way of looking at how skewed the S&P 500 market cap weighted index is (relative to equal-weighted). While the equal-weighted index has (by definition) 20% in the smallest 100 stocks of the index, the cap weighted is just 2% …meanwhile the top 10 swing a cap weight of 34% vs just 2% for the equal-weighted. This adds to the case and cautions for equal vs cap weight, and echoes the rotation theme.

Source: S&P Dow Jones Indices report

8. Deletions NOT Deleterious: Somewhat similar note, it turns out buying stocks that get deleted from the major stock indexes is a decent strategy. A basket of deletions would have outperformed the S&P500 handily. It again goes to show that sometimes it’s worth looking where others don’t, and doing what most won’t.

Source: Research Affiliates report via @TheIdeaFarm

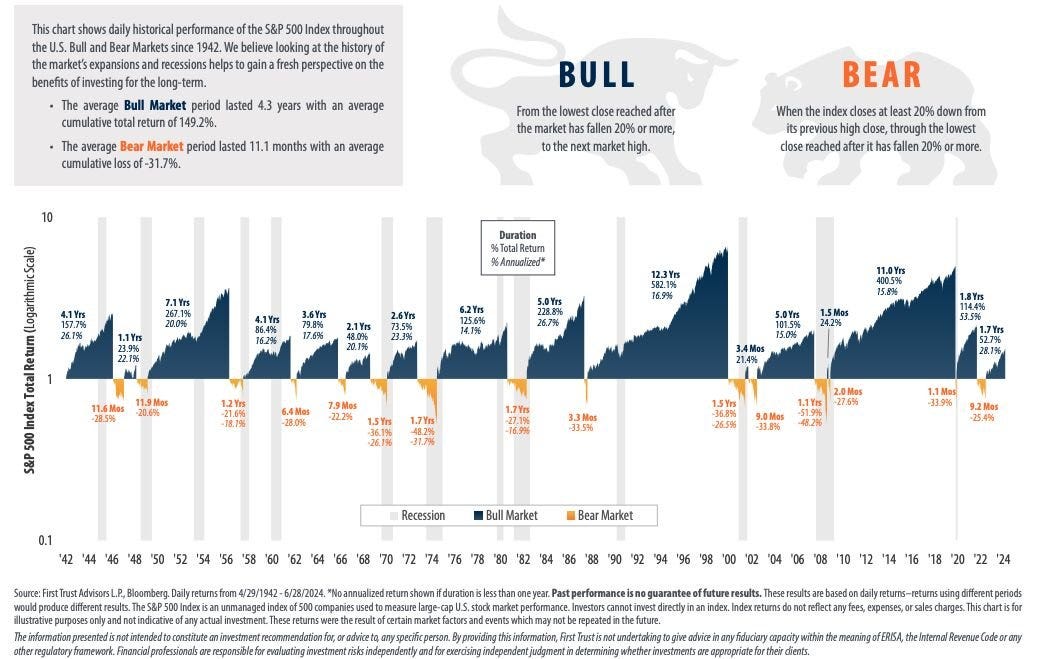

9. Bulls and Bears in Perspective: There may be some debate on how to define bull vs bear markets, and also an implicit nod to market timing by measuring these off the exact daily top/bottoms, but still interesting perspective here. The average bull market on this definition lasts 4.3 years and returns +149%, while the average bear market lasts 0.9 years and sees -32% declines.

Source: @MikeZaccardi

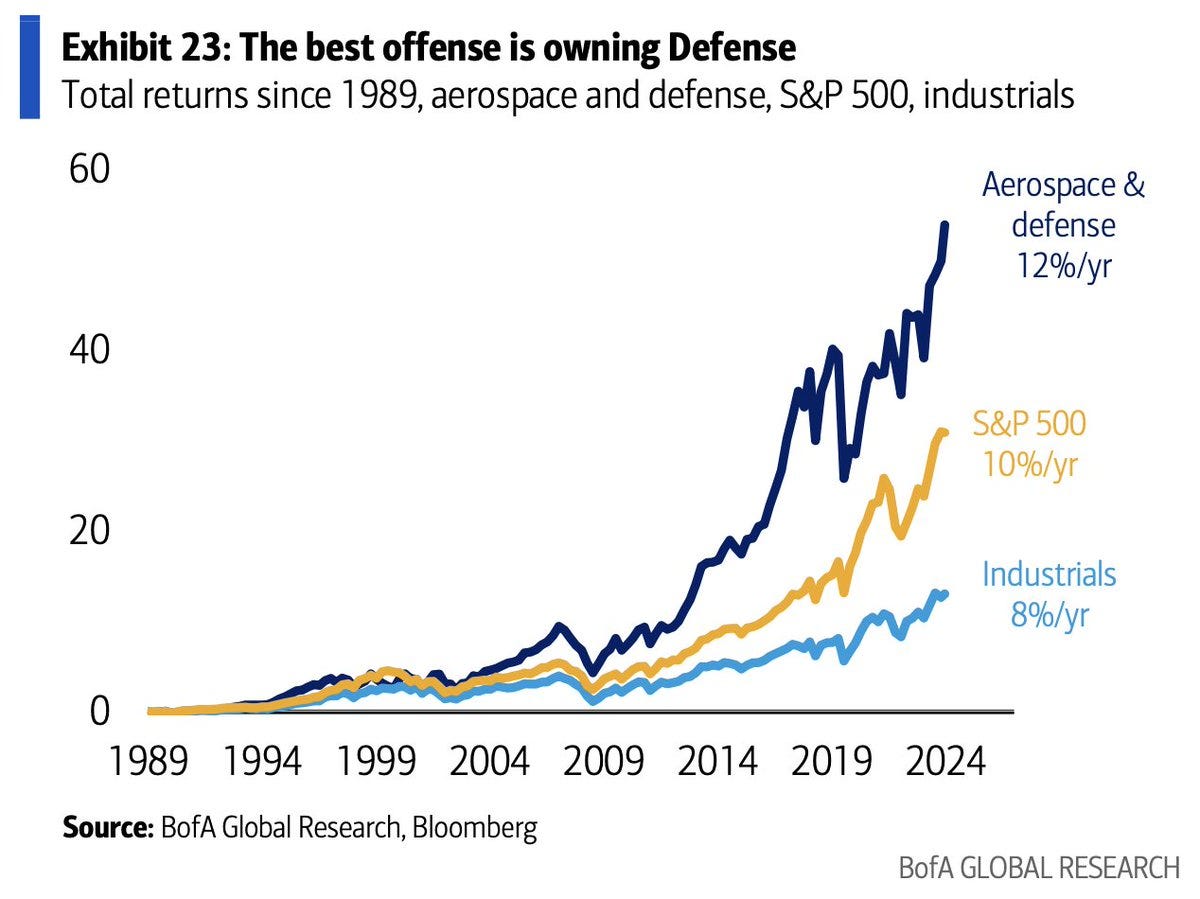

10. On the Defense: Longer-term, defense stocks have outperformed the S&P 500 — war is a racket. The idealist might point out the beneficent aspect of the aerospace side of things, and notably the rise of the space economy, but the pessimist would be quick to point out our warring ways, and the pragmatist would note that like-it-or-not it probably is a good defensive play in these increasingly fraught geopolitical times.

Source: @dailychartbook

Thanks for reading, I appreciate your support! Please feel welcome to share this with friends and colleagues — referrals are most welcome :-)

BONUS CHART >> got to include a goody for the goodies who subscribed.

Seasonal Uptick in Seasonality Commentary: here’s a quick look at the monthly seasonality stats table, this one covering all years — September does boast the worst stats. It has the lowest (and negative) average returns, and the lowest probability of gains. But…