Off-Topic ChartStorm - Sell in May?

No (don't do it), until you have checked out these charts...!

Here’s a quick Off-Topic ChartStorm on the “Sell in May” effect (10 charts on seasonality statistics and repeating patterns in markets).

Unlike the usual weekly ChartStorm (which focuses on the S&P500 and related issues), the Off-Topic ChartStorm is a semi-regular focus piece with topics spanning macro, markets, stocks, stats, commodities, regions, and various other issues of interest.

Learnings and conclusions from this session:

The May-Oct period tends to see lower, more volatile returns.

However only bear markets tend to see *negative* returns.

The Nov-Apr period tends to see higher returns.

The Sell-in-May effect is cyclical/changing.

The return spread is shrinking over time.

Overall, there’s a bunch of nuance and caveats to the worn-out old saying of “Sell-in-May” (which is by the way a shortened version of “Sell in May and go away, come back on St. Leger's Day”). Technically markets do indeed fare worse during this May-Oct period, but there are exceptions to the rule, and context is key. I always say when it comes to seasonality you ought to look at it last… as conviction building and confirming evidence to an existing robust thesis — not as the main thesis itself.

1. Sell in May? First of all, what even is this “sell in May” thing? As the seasonality chart below shows, May-Oct tends to be messy in markets — returns tend to be choppier, smaller, and volatility tends to drift higher.

So it does seem to be a worse time of the year for markets all else equal.

Source: Topdown Charts Topdown Charts Professional

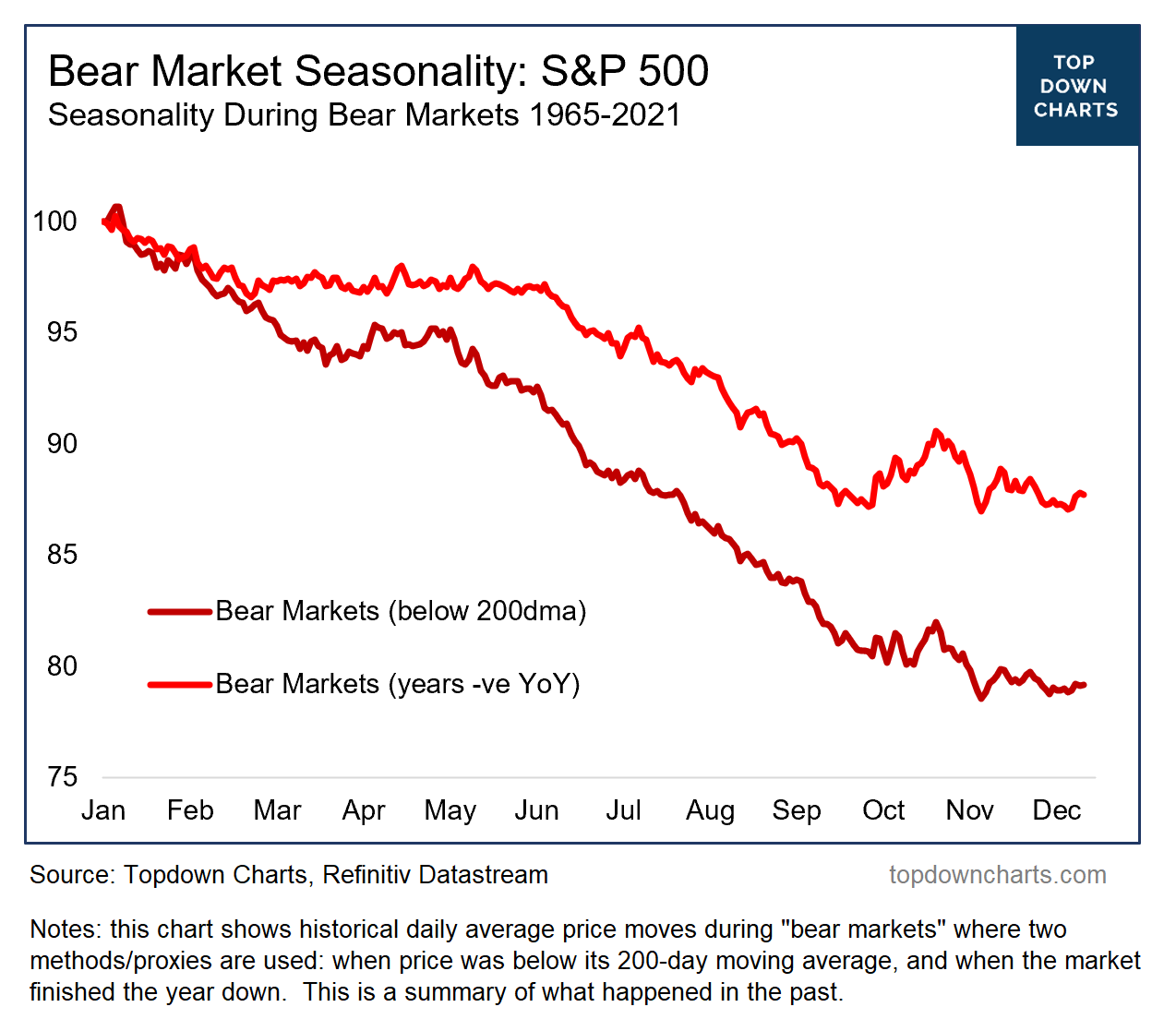

2. All Else is NOT Equal: Look at this chart from a post I did on conditional seasonality (how does seasonality look like in bull markets vs bear markets).

It turns out that this sell-in-May effect seems to be a bear market thing (by contrast, the green line keeps going up during the May-Oct period, albeit maybe a little more choppier than the Nov-April period).

The takeaway being: only sell in May if it’s a bear market.

Source: Chart of the Week - Bear Market Seasonality

3. But How will I know? The chart above uses 100% perfect hindsight to know whether it was a bull/bear market (did the market go up or down?), we don’t have that.

What we do have though is the 200-day moving average as a proxy (price above vs below), and it does a decent job (and if anything, reiterates the point that Sell-in-May is definitely a thing during bear markets).

Source: Chart of the Week - Bear Market Seasonality

4. But what about Probabilities? Is a question you should ask — because seasonality analysis like the above is just an average, and we know that averages can get skewed around …and probability (at least historical realized probability) is also important to know.

During bull markets the probability of a positive return was lower during the May-Oct months than the Nov-Apr months. Bear markets saw much lower probability of positive returns during May-Oct months (but also bad Jan/Feb).

5. What about for the entire May-Oct vs Apr-Nov periods? The Sell-in-May (SIM) period of May-Oct consistently underperforms the Buy-in-Nov [BIN] period… but only has a negative historical average return during bear markets

Again the proxy for bear market is above/below 200-day moving average — so in this case the analysis asks “was the index above or below its 200-day average at the end of April?” for the Sell-in-May measurements.

What’s interesting is that even during bear markets, while average returns were lower during the SIM period, the probability of a negative return was only ~45%. Also interesting is that the BIN period during bear markets outperformed the SIM period during bull markets. So SIM beats BIN, but SIM only really sucks during bear markets. Maybe we should call it Sleep-in-May (snooze in summer?) !!

Another thing to think about is if you were going to go try and time the market using the Sell-in-May effect (i.e. by going to cash during May-Oct, going fully invested Nov-Apr), with a historical average return of 2% during bull markets in the May-Oct period — you would need to be earning more than 2% in cash during the time you were 100% cash to avoid underperforming over time vs just Buy-and-Hold (cash rates would need to be and stay high: at least 4% when you went to cash… and this is ignoring dividends!).

ALSO: note that even in the best period in bull markets, it’s still only 75% positive… so 1/4 times the Nov-Apr period turned in negative returns even during bull markets.

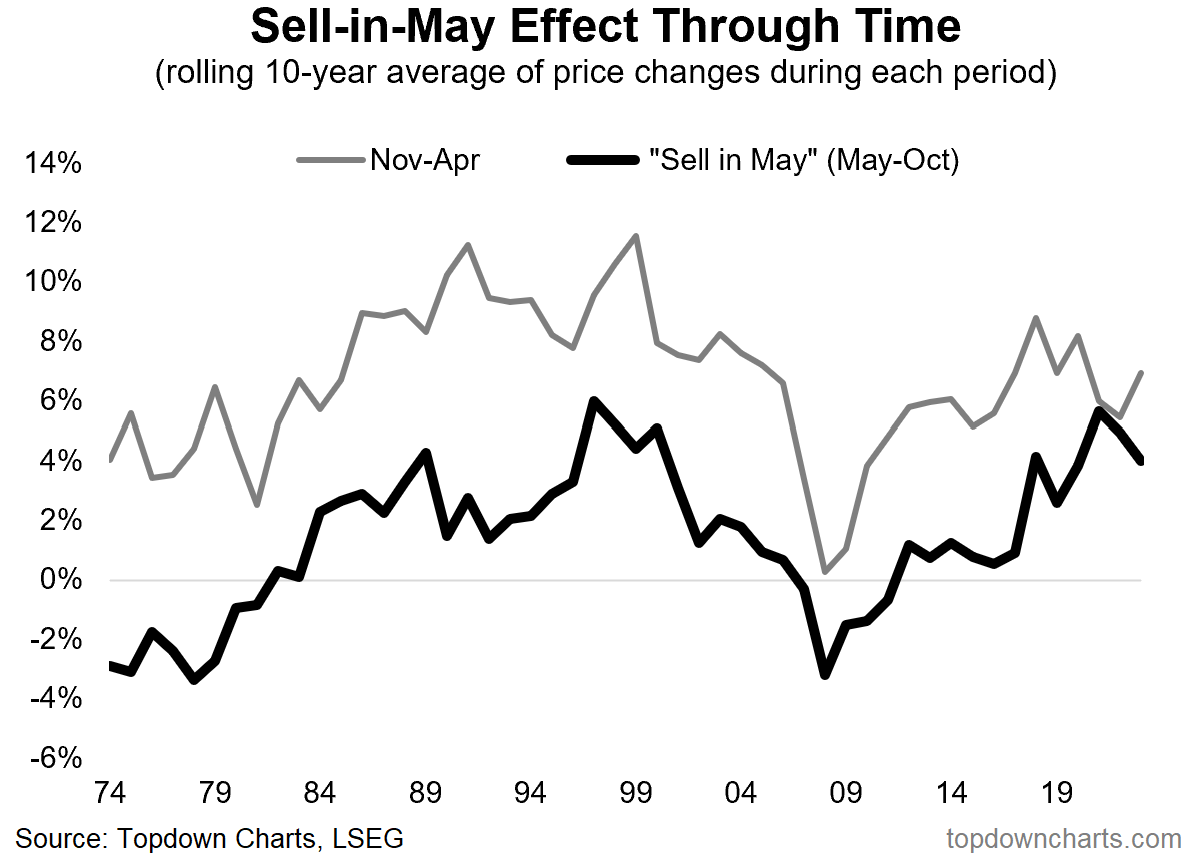

6. Does the effect change over time? I’m glad you asked, because it definitely does!

It seems to be cyclical, also the gap between the two periods is shrinking over time.

7. OK, any reasons or any other color? Well, economic data surprises tend to be worse in the May-Oct period, and better in Apr-Nov… and investor sentiment also tends to follow a similar pattern.

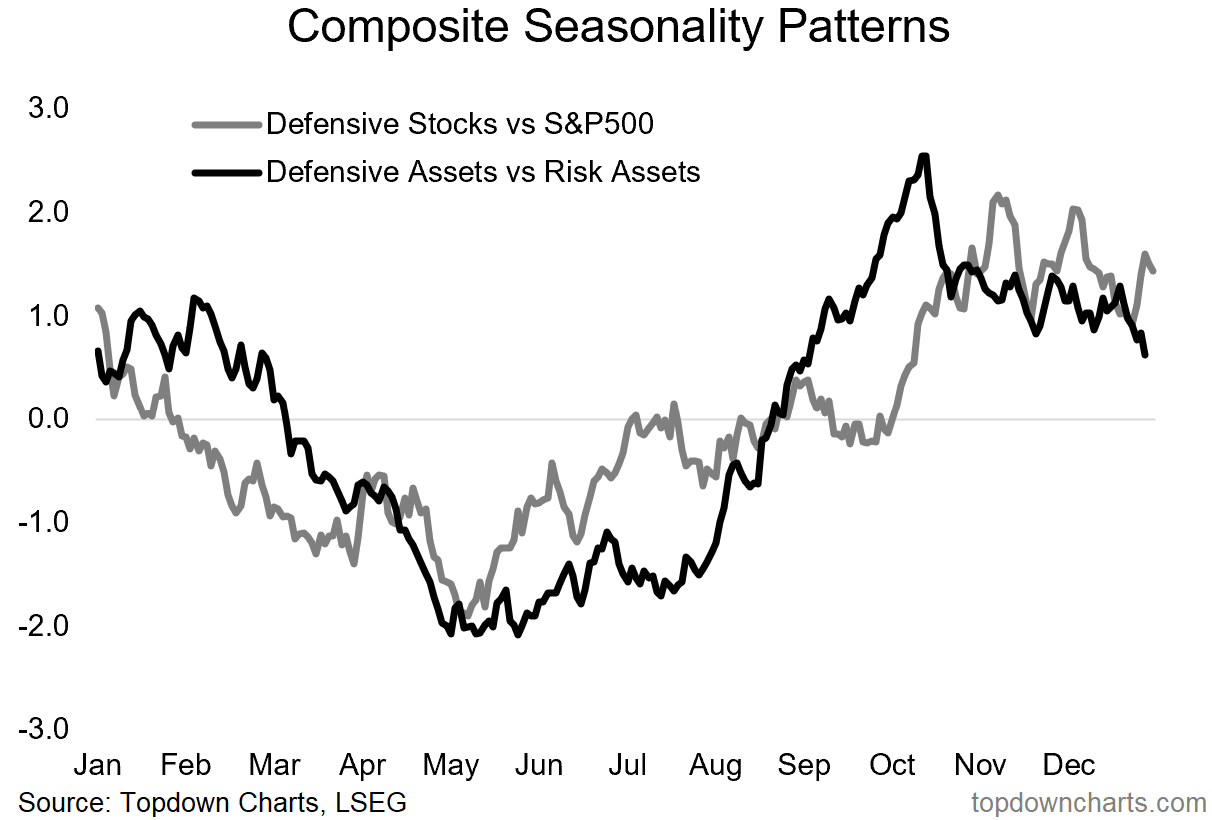

8. Other Assets? Defensive assets tend to do better in the May-Oct period (as you might suspect, given the worse sentiment/data/stockmarket returns during that time).

To clarify we are looking at the seasonal pattern of defensive stocks relative performance, and the spread of seasonality patterns for treasuries/gold vs stocks/VIX/credit spreads.

9. Even credit spreads? Yep, credit spreads tend to widen over the May-Oct period (and yes, even if you exclude 2008).

10. What else? The US Dollar (DXY) tends to weaken, and WTI Crude Oil trends higher during the murky May-Oct period.

Source: Topdown Charts Topdown Charts Professional

Thanks for following, I appreciate your interest!

Looking for further insights? Check out my work at Topdown Charts

Fascinating and it makes sense to reduce risk when people are away as information networks fracture.

What a comprehensive look at the SIM and BIN phenomena! Thanks Callum.