12 Charts to Watch in 2022 [Q2 Update]

An update to my post from earlier in the year (updated charts + comments/outlook)

As a departure from the usual Weekly S&P500 ChartStorms, and as promised, here’s an update to my 12 Charts to Watch in 2022!

In the original article I shared what I thought would be the 12 most important charts to watch for multi-asset investors in the year ahead (and beyond).

In this article I have updated those 12 charts, and provided some updated comments on the outlook -- given the dramatic shifts seen during the past quarter.

[Note: I have included the original comments from back at the start of the year, so you can quickly compare what I'm thinking now vs what I said back then]

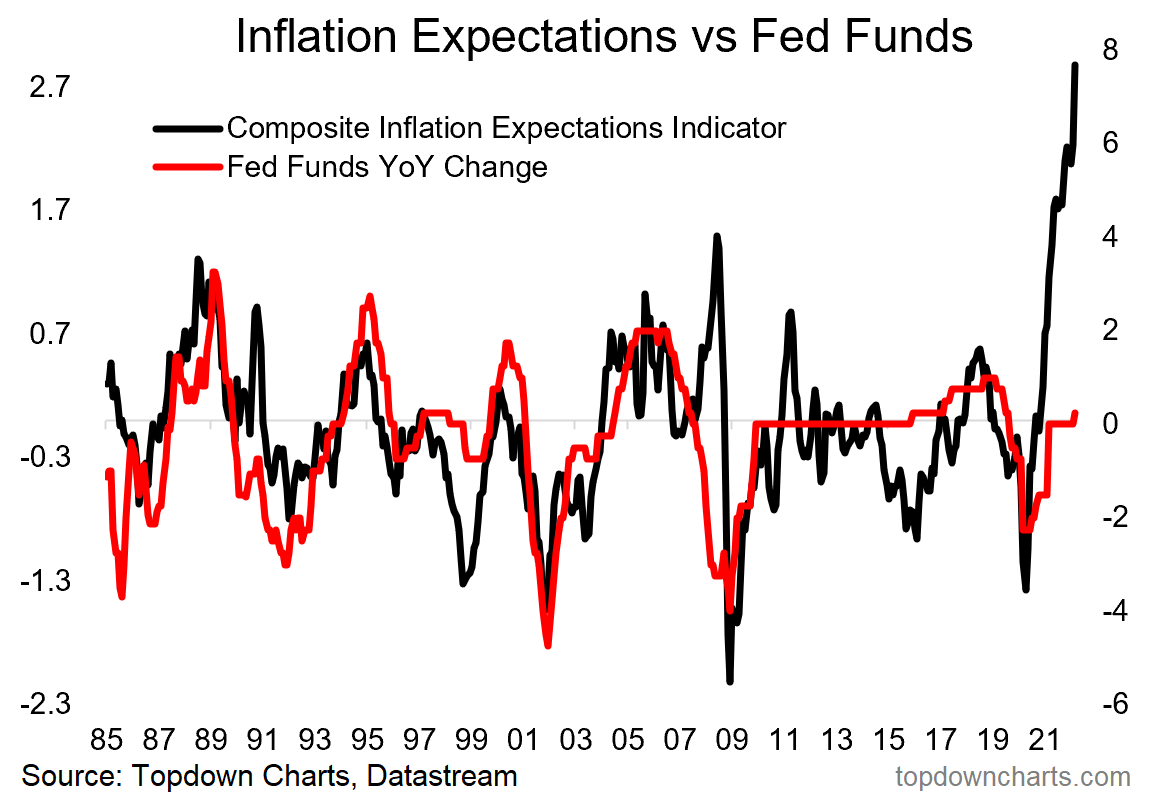

1. Fed Behind The Curve: This chart has perhaps become the most important chart of the current macro moment. Inflation expectations have spiraled to 40-year highs, and are at risky of anchoring at persistently high levels. Meanwhile the Fed has now pivoted resolutely into catch-up mode and is talking up the prospects of an aggressive rate hiking and balance sheet normalization program. How this chart plays out will ripple across nearly every asset class.

"Based only on this chart we could make an assertion that the Fed has fallen behind the curve. Against that there is the argument that other factors are important too, and not to mention the point that the Fed basically decided to position itself behind the curve to try and prevent the mistake of tightening too soon. With the composite measure of inflation expectations at 40-year highs it’s fair to suggest that the Fed may have some catching up to do as it kicks off the transition away from easing."

2. Fed Catch-Up Risk: Fed rate-hike lift-off means catch-up risk is in play. Credit has taken a hit from rising bond yields, especially the longer duration pockets of credit. But so far credit spreads have remained contained. And contained they will remain until something breaks, and it will: sooner or later.

"Naturally the Fed now faces another risk – i.e. the risk of being dragged into a game of catch-up in the context of a very complacent market that has arguably come to expect permanent easing... “the Fed has my back”. Just remember, the old saying of ‘don’t fight the Fed’ means don’t fight against the tides, and the tides are starting to change."

3. Growth Scare 2022: This was a simple scenario and something to ponder at the start of the year, but with the Ukraine war and ensuing geopolitical shockwaves, and the covid resurgence in China, a growth scare or outright downturn now seems likely. Multiple charts of leading indicators on my desk confirm this suspicion.

"But then again, maybe the Fed won’t even get a chance to get a rate hike out the door if the chart below proves anywhere near accurate. This and a few other leading indicators are pointing to a possible growth scare in 2022. Maybe it will be one-and-done for the Fed? Or maybe any such growth scare only serves to extend the economic expansion further by triggering renewed stimulus. Certainly a risk and a key chart to keep on the radar."

4. Corporate Capex: But all is not gloom and doom, capex growth is starting to pickup. There remains a very real prospect of a multi-pronged investment boom given thematics, fiscal rebuild/recovery programs, and longer-term impacts of the pandemic (commodities, logistics, and supply chain resilience efforts).

"This chart hints at perhaps one of the most important themes I’ve been talking about over the past year – the prospect of a possible multi-pronged, multi-year investment boom. The chart below highlights the typical cycle leads and lags in terms of capex growth, and with easier funding conditions, booming corporate earnings, and a rebounding economy it’s likely that we see a generalized uplift in capital expenditure.

But as I’ve been highlighting in the reports there are a few particular sectors that are likely to see a surge in investment in response to surging prices – for example, the global shipping sector, and commodity producers. Both of which have seen capex languish for the past decade, and both of which have seen an effective windfall from the pandemic (i.e. surging shipping rates and commodity prices)."

5. Capacity Utilization: Indeed, capacity utilization remains tight, especially labor markets. Arguably the black line in this chart is constrained by supply/shortages. Either way, this chart reinforces the inflationary pressures that continue to build in the system.

"Another key impetus to resurgent capex is tightening of capacity e.g. measures of labor market capacity utilization are close to pre-pandemic levels. This will put upward pressure on pricing and present an incentive or signal to firms to lift investment.

But it also speaks to the inflation theme. While some of the short-term upward pressures on inflation are likely to pass (e.g. backlogs, base effects, the initial bounce-back), should we see further and sustained tightening of capacity utilization it will put upward pressure on the more core or underlying inflation pulse."

6. Government (and Green) Capex: Again, whether its infrastructure, climate, or indeed energy security, governments around the world are embarking on fiscal stimulus programs that span hundreds of billions - and will take multiple years to fully implement.

"To really drive it home, the capex/investment theme is not just about corporations responding to economic forces, it’s also about governments responding to the pandemic as well as social/political forces.

Specifically in terms of recovery/rebuilding fiscal programs which in many countries have been targeted at infrastructure. But also climate related infrastructure and investment – something that is definitely part of fiscal packages, but also part of shifting investor preferences. We’ve observed a clear trend of rising financial investment into clean energy sectors being followed by uplift in real investment. So altogether it’s quite interesting."

>>> n.b. these charts were featured in my 2021 End of Year Special Report. Click through for a free download of that report.

7. US Absolute vs Relative Valuations: One of the consequences of the Fed vs inflation chart has been rising bond yields: bonds are fixated on runaway inflation and the ambitious tightening program espoused by FOMC members. As such, the last pillar of support for equities is being removed. Previously the argument was that the PE ratio is very high but it's ok because interest rates are low. As we see with a squeezing equity risk premium, it's just plain expensive now. At the margin this means a downgrade to the risk/return outlook for equities (especially relative to bonds).

"Should all this talk of capex and investment booms come to pass, we’d likely start to see upward pressure on bond yields, and that will put a squeeze on the US equity risk premium.

The chart below is one of my favourites for thinking about US equity valuations. It points out what most of us already know: US equities are expensive in absolute terms …i.e. the PE ratio is really very high. But if we factor in low bond yields then maybe it’s not so bad. At present the chart says absolute valuations are wildly expensive, but relative valuations are ok (for now). That will change if/when bond yields rise – and in that sense it also goes to highlight the interest rate sensitivity of the market if we accept the statement that equities only offer reasonable value in a low yield environment."

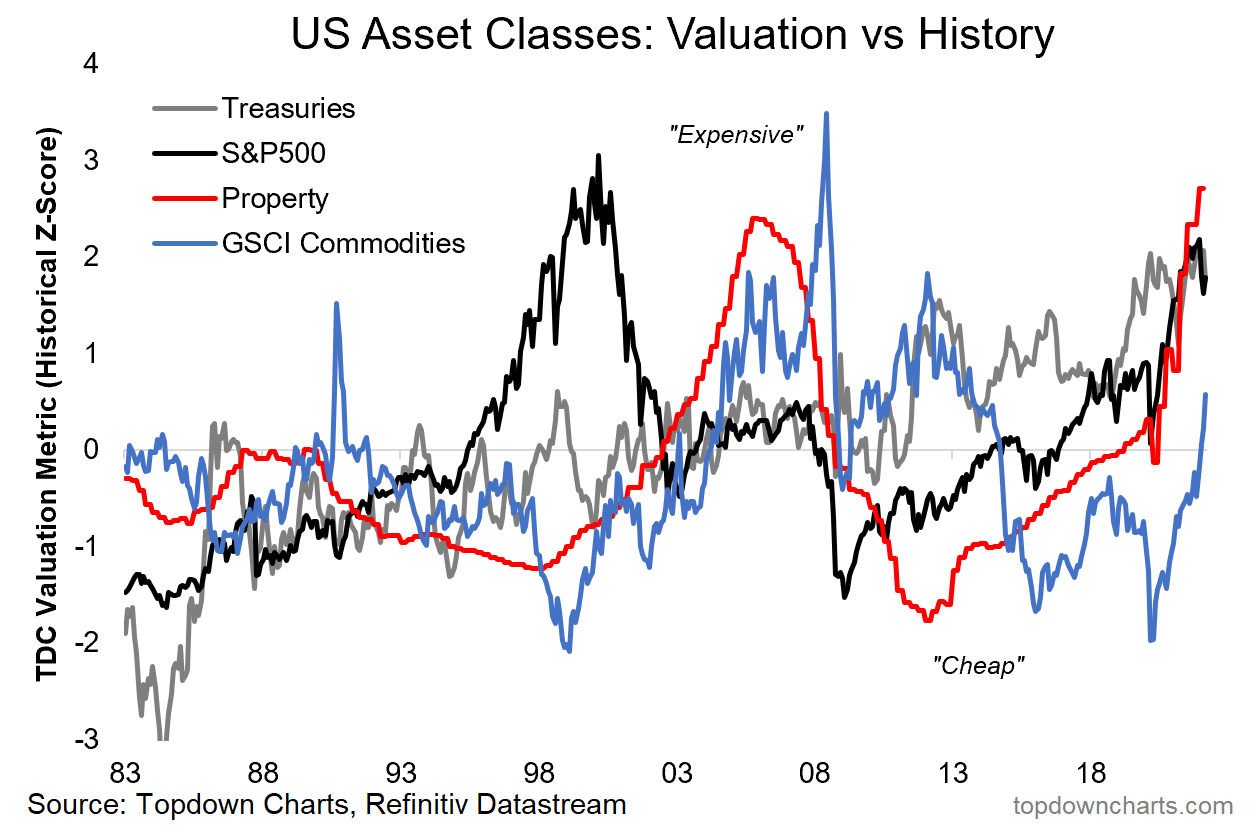

8. US Asset Class Valuations: But it's not just equities, it's also bonds, housing, and increasingly also commodities. When everything is expensive, maybe we could suggest that in that situation that only cash is cheap!

"To complicate matters slightly, my valuation metrics show bonds expensive vs history as well – so: “equities look reasonable vs expensive bonds??”. To make matters worse, property prices are also sailing into rarefied air. Commodities on the other hand, while not cheap, at least look reasonable by comparison and could benefit from increased capex."

9. US vs Global Equity Valuations: But peering into global equities we can certainly find *relative* value. Perhaps most interesting in the latest run of this chart is how developed markets have dropped down to match the valuations of EM equities. Pretty interesting when you consider the differing level of country/governance risk. The other thing to note again of course is that US equities look extremely expensive vs the rest of the world.

"Another chart that makes US equities look expensive by comparison is when you look at PE10 (or really just about any other valuation metric) for the US vs the rest of global equities. It is true that Emerging Markets and Developed Markets excluding the US have seen a decent rebound in valuations since the March 2020 lows, but there is a clear and compelling relative value case here."

10. Global Equity Super Sectors: The unique macro backdrop of 2022 and the tech-tumble has contributed on all angles to a big boost in relative performance of what I call the super sectors of "old cyclicals" and "defensives". Cyclicals in this sense got a big boost from commodities, while defensives performed true to label during the tumultuous market conditions so far YTD. I continue to think looking at global equity markets in this lens makes sense. Rotation is here.

"The most logical pushback on the previous chart is to note that we could have said something similar for much of the past 5-10 years. So, the question is then what will it take for this gap to close?

One avenue for a turn in relative performance of global vs US is the path of the “super sectors”. A big part of US outperforming the rest of the world has been the high hurdle set by tech and tech related companies. Global ex-US has a big skew to “old cyclicals”.

In that respect, the most important technical clues to a rotation in performance between US and global will be the chart below. Specifically look for an upturn in the blue line to get a jump on a ‘virtuous turn’ in US vs global relative performance (and value vs growth for that matter, also smalls vs large – it’s a fairly sprawling issue in equities!)."

11. Low Quality Credit – Low Risk Premium: Back on credit and sticking with valuations, the lower end of the credit quality spectrum continues to trade on very tight (expensive) relative valuations. Simply put, credit markets are not prepared for a downturn, and at this point look largely oblivious to the apparent storm clouds on the horizon.

"The valuation conundrum is not just the domain of equities – credit also is looking increasingly expensive. The chart that hammers the point home to me is this composite view of where the lower quality credits are trading relative to the higher quality credits. Basically we see a lower and lower risk premium for lower quality credit.

By itself this may not be an issue, particularly if the economic and monetary backdrop are supportive of credit conditions. But if credit conditions deteriorate things could turn sharply here – and indeed, we may well even see early clues of any impending stress in this very indicator itself. So very much one to keep checking in on."

12. China Property Downturn: Meanwhile in China the property market downturn remains in full swing, and the covid resurgence likely weighs further. The upside of the downside in the China macro pulse though is the prospect of more forceful easing. And if you are looking for upside risks or reasons for optimism then you'd do well to keep a close eye on this corner of the macro map.

"I always say in my many years of covering China macro, if I could only choose one indicator it would be property prices, and perhaps if I were to pick only one chart it might be the one below.

My composite leading indicator for Chinese property prices (money supply, interest rates, funding) is pointing to an extension of the current downturn deeper and well into 2022. This is of critical importance in so far as the economic pulse and commodity demand is concerned, but also – for the policy outlook: the lower that black line goes, the greater the probability of monetary stimulus (and you know what that means!)

Summary and Key Takeaways:

-The Fed has pivoted into catch-up mode as inflation expectations risk (/are) running away, expect a string of rate hikes and balance sheet normalization.

-The pivot from stimulus to stimulus removal and then tightening poses risks to just about every asset class: particularly in light of the complacency that still is clearly evident.

-(but) there are upside risks in the form of a possible multi-pronged capex/real investment boom, and eventual albeit stop-start reopening/normalization.

-(but!) there are also clear and pressing downside risks e.g. a likely global growth scare as stimulus gets removed, financial conditions tighten, and price pressure bites.

-Geopolitics & Covid resurgence have nearly cemented the slowdown thesis.

-A key issue with regards to a growth slowdown and monetary tightening is the reality of multiple major asset classes looking historically expensive (e.g. US equities, property, bonds, and even commodities).

-With many assets still richly priced in absolute terms, relative value remains the last bastion, and indeed rotation likely remains a key theme this year.

-Other than that, a defensive skew and eye on risk management seem prudent.

Overall: Heading deeper into 2022 the risk vs return outlook is clearly and steadily shifting across asset classes, and we’ll need to focus on both short and longer-term indicators to navigate risk as we progress through this strange -- but also somewhat familiar cycle.

Thanks for reading!

NOTE: this post is based on an excerpt from my 2021 End of Year Special report - click through to download a free copy of the report.

Sincerely,

Callum Thomas

Head of Research and Founder at Topdown Charts

Follow me on Twitter

Connect on LinkedIn

SPONSOR: ( …he’s me!)

My research firm, Topdown Charts, has a new entry-level Substack service, which is designed to distill some of the key ideas and themes from the institutional investment research service to provide the same high quality insights at a more accessible price and easier to digest weekly email.

Give it a try and let me know what you think!! :-)

great read thank you